How TV Informs My Financial Management Strategy

Two summers ago I gave our household a financial makeover. I spent the entire August long weekend sorting out our various financial papers and bills into piles while watching past episodes of Till Debt Do Us Part on the internet to use the scare tactics of Gail Vaz-Oxlade to whip me into shape.

Two summers ago I gave our household a financial makeover. I spent the entire August long weekend sorting out our various financial papers and bills into piles while watching past episodes of Till Debt Do Us Part on the internet to use the scare tactics of Gail Vaz-Oxlade to whip me into shape.

I knew we had some debt. I just didn’t know how much. I had a vague idea of what we owed, but I didn’t really want to know. The only thing I knew was that what we owed was scattered over three lines of credit and a home depot credit card.

I put it all together and it wasn’t pretty. We owed about $10,000 more than I estimated. Gulp! I’m going to be brutally honest as most people won’t share with you the actual amount, but we owed a little under $60,000 dollars in addition to our mortgage.

My Till Debt Do Us Part marathon taught me that in one school of thought that debt can be classified as ‘œgood debt’ and ‘œbad debt.’ A debt can be good if you to apply the basic principle of future value. As Vaz-Oxlade educates, ‘œIf the future value of the item you are buying can reasonably be thought to be higher than the current value, you’re likely taking on good debt. If the future value will be less ‘” if the item will depreciate ‘” that would be bad debt.’

When I looked at what made up that horrifying sum, I was completely horrified, but I was also happy to see that most of our debt was of the good variety. Not necessarily the smart variety, but it was so-called ‘œgood debt’ nonetheless.

Here’s a quick breakdown of how we spent our yet-to-be earned cash:

- $20,000 to buy our house (we borrowed from our lines of credit to deposit into our RRSPs which we withdrew 90 days later to use as part of the down payment on our house)

- $23,000 to waterproof the foundation of our house (turns out we bought a dud with a leaking basement, more on that some other time, but I’m going to argue that this won’t negate the future value of our home in some far off future)

- $7,000 to fund a kitchen renovation

- $10,000 most likely residual costs related to buying the kids furniture and clothes when they moved in and the 7 month unplanned parental leave

We were overwhelmed, scared and angry that we had done this to ourselves. We’re also an action oriented couple and decided to make a plan to be debt-free in five years. Once we decided, and were okay with, that financing our retirements, childrens’ educations, savings and fun things like vacations weren’t going to be our priorities, we were clear and focussed on what needed to be done.

Our single financial goal is to pay off our debt.

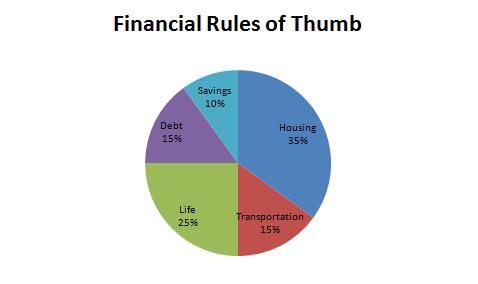

Using Vaz-Oxlade’s formula for financial health, we set up a household budget on excel to prescribe to the following formulas. Whatever your annual net income, expenditures are not to exceed the following ratios:

This works for us relatively well. We’re a one car family and we live in a city, so our transportation expenses are much less than the recommended 15%. We’ve even managed to get our housing expenses down to around 30% due to my energy frugalness and ability to tirelessly sing ‘œsaving energy, turning off the lights when you leave the room’ to our two children.

With that little bit of savings, we’re able to increase our monthly debt repayment and have for sanity purposes upped the amount of money we spend on the life category.

Do I really need the city newspaper delivered to my house with the attached subscription cost of $24.89 a month? The answer is no. However, our 11 year-old son has finally discovered reading. He’s evolved from looking at pictures to reading text and spends 30 minutes every morning devouring the comics that it makes it entirely worth every penny.

I come to this because my last Queercents post sparked some really interesting comments that I’ve been grappling with in my head. Essentially I’ve been mulling over and over the question ‘œHow do the financial choices you make in today (for me, in my thirties) affect you down the road (for me, in my forties)?’

I’m still not sure…yet. But this big disaster that we created and are currently cleaning up is certainly impacting our lives today.

We have a plan, we’re making progress, but it’s not always easy. Every now and then, I need a tune up. I do fall off the rails because I forget the ultimate goal and end game.

That’s when I fire up the laptop and watch more episodes of Till Debt Do Us Part. There’s nothing like projection and spending time with the ghost of your financial future to quickly quell bad habits.

Photo credit: stock.xchng

Share this:

Discover more from Queercents

Subscribe to get the latest posts sent to your email.

Holly: Thanks for the post and your candidness. A lot of people might not fess up to the number. This level of sharing reminds me of a New York Times article that highlighted debt bloggers and how online exposure gave them the discipline to reduce their debt.

Also, as regular contributors for Queercents, it makes us more aware of personal finance in general and hopefully, this experience will help you keep your debt reduction plan top of mind! I look forward to reading more about your progress and how you’re paying down the debt!