The Three-Minute Portfolio

“The perfect is the enemy of the good” — Voltaire

“I’m finally ready to begin investing, but I don’t know where to begin. Stocks. Bonds. Mutual funds. ETF’s. It’s all very confusing. I have some cash in a savings account, but I want my money to work harder. What do I do?”

The premise

Getting started with an investment portfolio doesn’t need to be difficult. The following steps will take you to a solid, low-cost, easy-to-maintain portfolio. You might not end up challenging Warren Buffett for the title of World’s Best Investor, but you’ll sleep well, and you won’t spend every waking hour worrying about your investments.

Well-managed index funds have low expense ratios, since you’re not paying anyone to scout out the world’s best companies. All the manager does is maintain a portfolio of stocks or bonds as indicated by the index, whether it’s the S&P 500 or the MSCI EAFE.* Mutual funds (including index funds) give you a little bit of ownership of hundreds of companies. If one company stumbles, you won’t lose too much money; conversely, your returns are not going to “hit it out of the park.” The idea is to move up and down with the market, with the assumption that in the long run, there will be more up than down.

In addition to spreading out the risk over hundreds of companies, you also want to spread it out over the world. Having some money in foreign investments helps you take advantage of productivity improvements made in other countries and gives you some protection from the falling dollar.

You’ll also want to have some money in bonds as well as stocks. Individual bonds have a pre-determined rate of return, and a portfolio of bonds (such as a bond index fund) has much less volatility than does the stock market (OK, maybe not in 2008-2009, but it was the great exception).

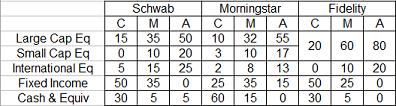

Asset allocation is the art of deciding what percentage you want to assign to each category of investment. In a previous post, I wrote about the different recommendations found on three major websites: Morningstar, Schwab, and Fidelity, for conservative, moderate, and aggressive investors. Each site has a different method for calculating the return of a hypothetical portfolio, leading to significantly different conclusions about the optimum portfolio composition. You can agonize over it, or you can just pick something sensible. “Sensible” should include your time frame for needing the money (the sooner you need it, the higher the percentage in bonds or cash) and your tolerance for risk (the lighter you sleep, the more you should be in the lower-risk bonds or cash).

Low expense ratios

The expense ratio of a fund is the percentage of the fund assets kept by the fund managers for maintaining the mutual fund. Expense ratios for index funds can be as low as 0.09%; whereas, an actively-managed emerging market fund might charge as high as 2.5% (or more). Fund managers pay themselves first (surprise!). So if they made 7% on their investments, the 0.09% index fund will give you 6.91% and the other will give you 4.50% — which would you rather have? Of course the theory (and the sales pitch) is that the highly-managed fund pays for the best minds to find the world’s hidden gems. It works that way sometimes but not often. Low expenses are more likely to reward the long-term investor.

The process:

- Pick a brokerage: Schwab, Vanguard, Fidelity, or E-Trade (or any other brokerage, but then you’re on your own).

- Pick an asset allocation: conservative, moderate, aggressive, or something in between.

- Enter the total amount that you will be investing.

- Multiply the total by the percentage for each asset category.

- Voila! You’ve found how much to invest in each of four specific funds.

Step-by-step:

Pick a brokerage. Choose one that offers many mutual funds with low expense ratios, no transaction fees, and low minimums. If you like face-to-face interaction, choose one that is convenient for you to visit. Schwab and Fidelity have offices around the country. For mutual funds, Schwab and Vanguard are the classic choices. Vanguard only offers their own mutual funds, but they are some of the best. Vanguard charges an annual maintenance fee of $20/fund for each fund with a balance below $10,000 unless you sign up for on-line statements. (So sign up for on-line statements). Schwab enables you to hold stocks, too, and has low stock transaction fees. Fidelity has higher minimums than Schwab or Vanguard. Mostly, it comes down to personal preference.

Pick an asset allocation. Below is the table from my previous post on asset allocation recommendations from Schwab, Morningstar, and Fidelity. Columns C, M and A show percentage allocations for conservative, moderate and aggressive portfolios. If you’re nearing retirement, choose an allocation on the conservative side. If you have a long time frame, you can slide it towards the aggressive side, but be aware that more risk does not necessarily mean more reward.

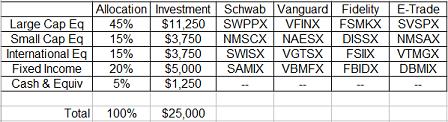

Enter the amount to invest, and multiply by the allocation: The table below shows an example of a $25,000 portfolio, divided into five asset categories: US Large Cap Equities, US Small Cap Equities, International Equities, Fixed Income (Bonds) and Cash & Equivalents (e.g. Certificates of Deposit). The allocation in the first column is chosen to be in between Morningstar’s recommendations for a moderate and an aggressive portfolio.

Three-Minute Portfolio Fund Picks: The funds listed for each brokerage were selected for the following: expense ratio < 0.5%, no load and no transaction fee, fund size > $50M, fund existence > 5 years, bond funds are not municipals (munis are most advantageous for high income folks), 3-5 Morningstar stars (5 is the highest; most index funds rate 3), minimum initial purchase < $3,000. More fund details can be found here about which index each fund tracks, expense ratios, and account minimums.

Three-Minute Portfolio Performance: The graph below is the portfolio’s performance as calculated on Morningstar. (Morningstar has great free stuff.) In the good times, the index (light gray line) goes higher than the portfolio, but in the bad times the portfolio doesn’t go as low as the index. The portfolio is buffered through diversification.

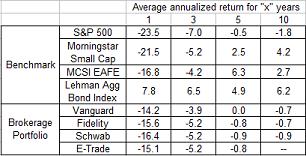

The table below compares the performance of the portfolio at each of the four brokerages. Since they are invested in index funds, with approximately the same expense ratios, tracking the same indexes with the same weightings, it’s no surprise that the performances are also relatively similar.

Why index funds instead of ETF’s? Well-managed exchange-traded funds (ETF’s) also have low management fees, but they have transaction fees. Buying shares in an ETF is like buying stock — you pay the brokerage for each purchase and each sale. With no-load no-transaction-fee mutual funds, there are no such fees. Schwab, for example, charges $12 per ETF or stock transaction, so to set up your four-fund portfolio would only set you back $48 — not too bad.

But the next step is to start contributing regularly, e.g. monthly, to your portfolio. I’ll write about this in a future post. There are significant benefits to dollar-cost averaging. And you should periodically rebalance your portfolio — a time-tested low-risk technique to improve your returns. (Also a future post). Growing and maintaining your portfolio will mean additional transactions, and while $12 may not sound like a lot, it can really add up to a significant fraction, especially if your total portfolio is relatively small.

Don’t fall prey to analysis paralysis. Just go do it. You don’t have to use my fund recommendations. I put together my short list to demonstrate:

- You don’t need to select many funds, and

- You don’t have to find the perfect fund.

But don’t let your nest egg wither in a savings account. (Do keep your emergency fund there.) If you’re expecting your investments to help provide for your golden years, you better put them to work.

Disclaimers: This information is provided for educational purposes only. It may not be an appropriate investment for you. Learn all you can about investing before plunking your money down. Investments in mutual funds are not FDIC insured and can cause loss of principle (you can lose money).

*MSCI EAFE = Morgan Stanley Capital International Europe, Australasia, and Far East.

Image credit: Erica Marshall on Flickr

By day, Helen engineers new materials to make computer chips cheaper, better, and faster. When the son goes down (pun intended), she writes about personal finance at Affine Financial Services.

Helen, this makes much more sense to me than what the investment adviser at my bank told me – probably because of the visual aids.

This question might be totally off topic (and if it is, I apologize), but what is your opinion of mutual funds that only invest is socially responsible companies? The guy at the bank said that it’s a really low rate of return and he didn’t recommend them. But I hate the idea of my money being used to drill for oil in ANWR or to support companies like Wal-Mart who have poor employment practices.

Hey Serena,

Glad the vis aids helped. Thanks for your help in formatting them — I think the layout is much improved.

I think that sleeping well is priceless (to paraphrase a commercial). And if it’s important to you to know that your money isn’t being used for whaling and deforestation, then it’s important. No sense giving up your principles for a little principal.

One challenge can be finding a fund that has the same definition of “socially responsible” as yourself. Some folks don’t like nuclear power, others gambling or oil. There’s a great website: Socialfunds.com to help identify some potential investments for you.

You might check out APPLX (Appleseed Fund). Pros: No load. On a hot streak. Great review in Morningstar. Cons: A bit concentrated (60% of assets in to 10 holdings). Only been in existence for a few years.

Or DFESX (DFA Emerging Markets Social Core Equity) for socially responsible large cap emerging markets (think Thailand). Pros: Good performance. No load. Low expenses. Cons: Also relatively newcomer.

I didn’t investigate these “picks” very much (so take the advice with a grain of salt) — just wanted to show that there are some good funds to consider.

Hey Helen – Thanks for the follow up. I’ll definitely check out those funds you mentioned.

Your point about emerging markets brings up another question about ethical investing – I guess it all depends on what side of the development debate you fall on whether you think investing in foreign countries is a good idea or not. But in terms of diversification, I totally see the logic.

This is extremely timely information – I’m struggling my way through about a million (ok, 330, but still) mutual funds I can purchase through my 403(b) plan at work. I’ve been keeping my head in the sand but next week is the sign-up deadline – yikes!

I’m going to sit down with the big scary book and this post tonight and just….pick.

Jenn:

Big scary book, indeed! It’s great that your employer offers 330 investment choices — or maybe not. Some choice is good. Too much can be overwhelming.

I have some friends from Russia. The first time they entered an American supermarket they were completely overwhelmed. It was very difficult for them to re-learn how to shop (by now, of course they are the same spendthrift consumers as the rest of us.)

Let me know how your selection goes. If you get it down to a final four (or sweet 16) and want a second opinion, let me know.

Good luck,

Helen.

Hi Helen:

We have 14 providers, each with their own enormous portfolios – seems to be designed to innundate you with choices and keep you out of the system. I feel roughly like I do in the toothpaste aisle – so many differences without significant distinction.

Thanks for the offer. I may well let you know. I’ve got a date with my dad/financial advisor tonight too….

Warmly,

Jenn